On May 28, the fourth online event in the Energy Security Talks series took place: What Will the Situation in Ukraine’s Energy System Be Like This Summer? During the event, the DiXi Group think tank presented its analytical reviews titled Summer Outlooks: Assessment of the Gas and Electricity Market Situation Ahead of High-Demand Seasons and Strategic Reserves Formation Periods.

The documents were developed based on the methodologies of the European Network of Transmission System Operators for Electricity (ENTSO-E) and Gas (ENTSO-G), adjusted according to available open-source data and adapted to the conditions of martial law. The analysis allows for the assessment of existing risks and the preparation of proposals to strengthen the resilience of Ukraine’s energy system.

Based on this analysis, DiXi Group formulates recommendations for the government, businesses, and international partners aimed at improving crisis preparedness, effectively utilizing international financing, and accelerating integration with the EU energy market.

Roman Nitsovich, Director of Research at DiXi Group, emphasized during the opening of the event:

“We believe that assessing the sufficiency of energy resources is not only a technical task but also a socially important tool that helps the country better prepare for potential crises and maintain resilience amid uncertainty.”

Summer Outlook (Electric Power Sector)

Olena Lapenko, General Manager for Energy Security and Resilience at DiXi Group, presented a short-term and seasonal assessment of the power system’s adequacy, including the current state of the sector, consumption dynamics, import dependence, and a forecast for the summer of 2025.

According to the expert, all assessments are approximate and based on an analysis of trends over the past three years. Analysts compared data from before February 24, 2022, with current open-source data to identify key changes and patterns and to develop corresponding forecasts.

State of the Power System

Currently, the backbone of Ukraine’s power system remains nuclear generation, which produces the largest share of electricity. The overall generation structure has not significantly changed compared to pre-war years; however, available capacity has decreased due to infrastructure damage.

Partial recovery is underway — 4 to 5 GW of capacity has already been returned to the system. Thermal generation capacity stands at about 4.5 GW, and hydroelectric capacity is nearly 4 GW. At the same time, hydro resource utilization is limited due to the absence of spring floods, and the summer period traditionally coincides with active maintenance campaigns at thermal power plants. Additionally, 2 to 3 nuclear power units will be under maintenance, reducing the total available capacity by 1.3 to 1.4 GW.

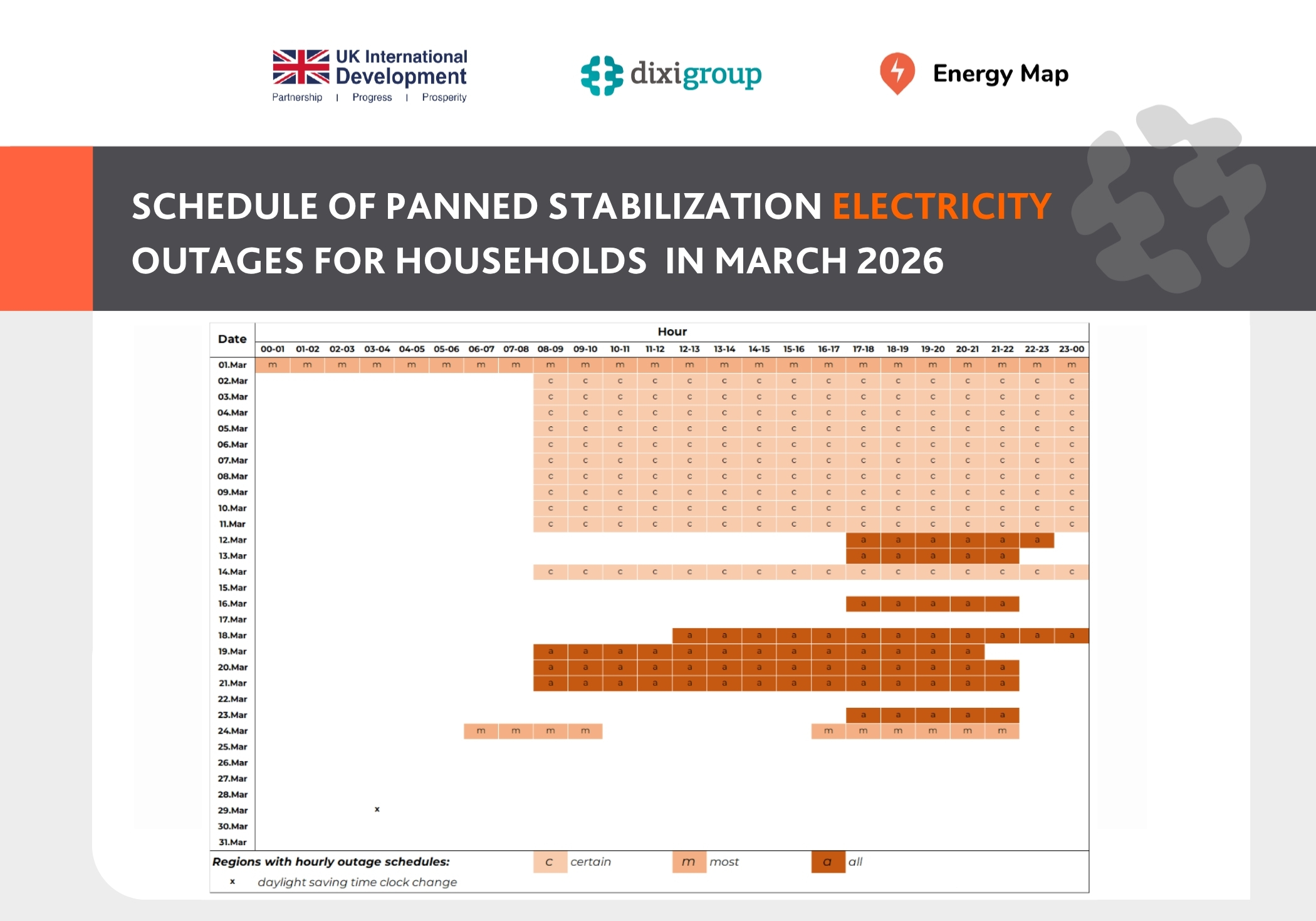

The most challenging situation is observed in frontline regions, where regular attacks by the aggressor country disable network equipment, causing power outages for consumers.

Consumption

Since the start of the full-scale invasion, Ukraine has shown a steady decline in electricity consumption by industrial consumers. The reasons include destruction of production facilities, occupation of part of the territory, and reduced working capital for businesses. According to DiXi Group estimates, electricity consumption in 2024 decreased by 3–6% compared to 2023. Given the mild winter and lower demand, this trend is expected to continue.

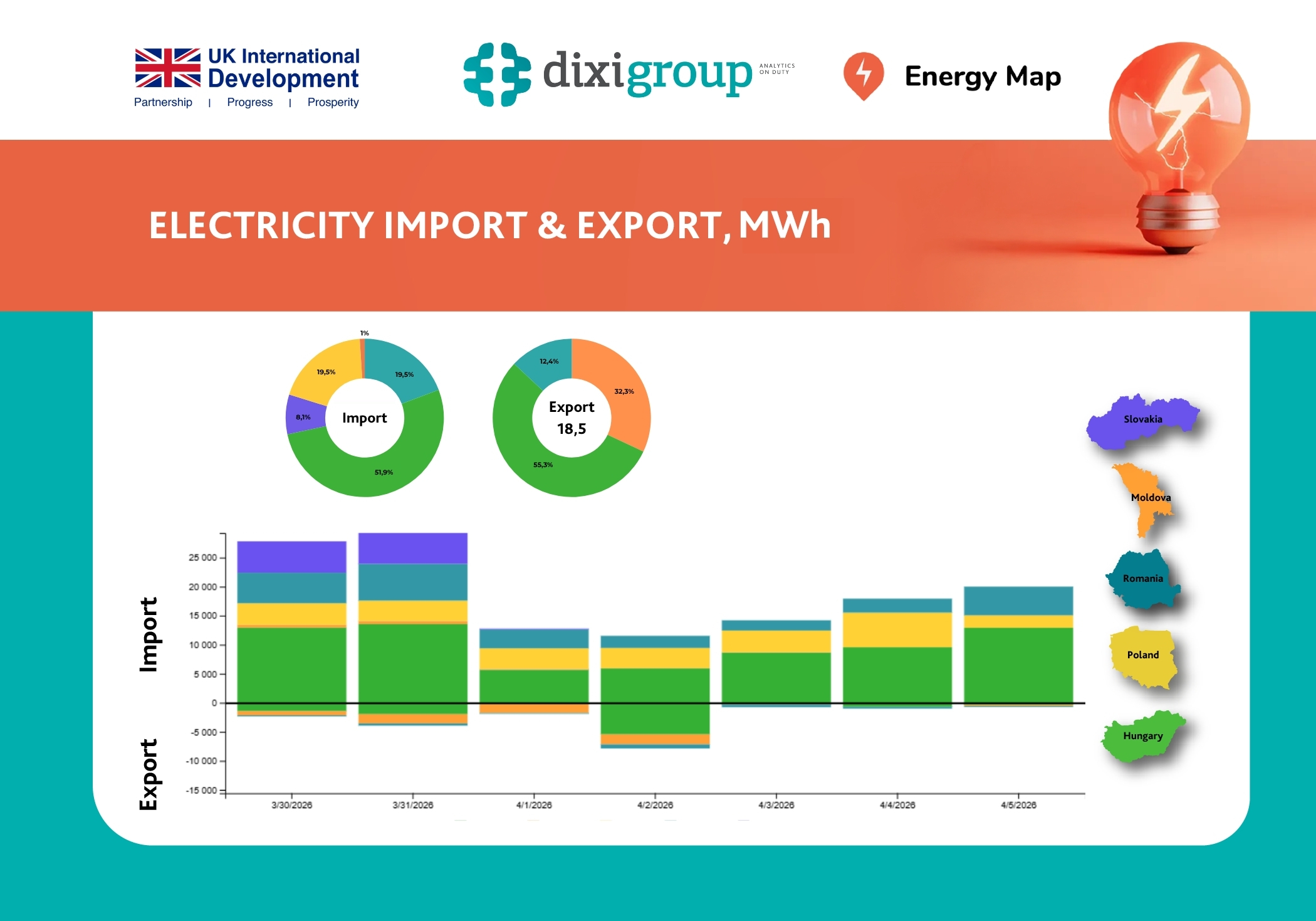

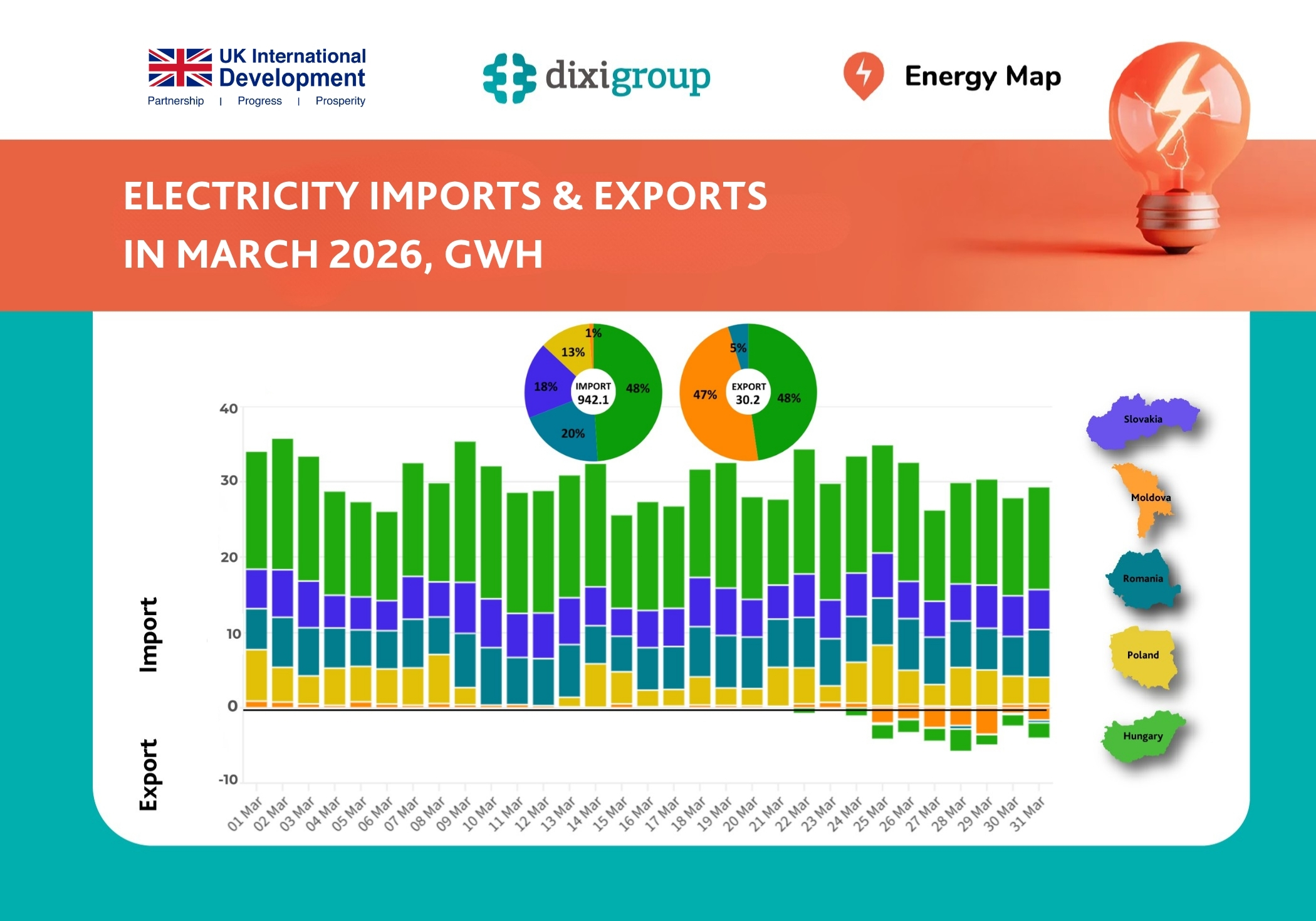

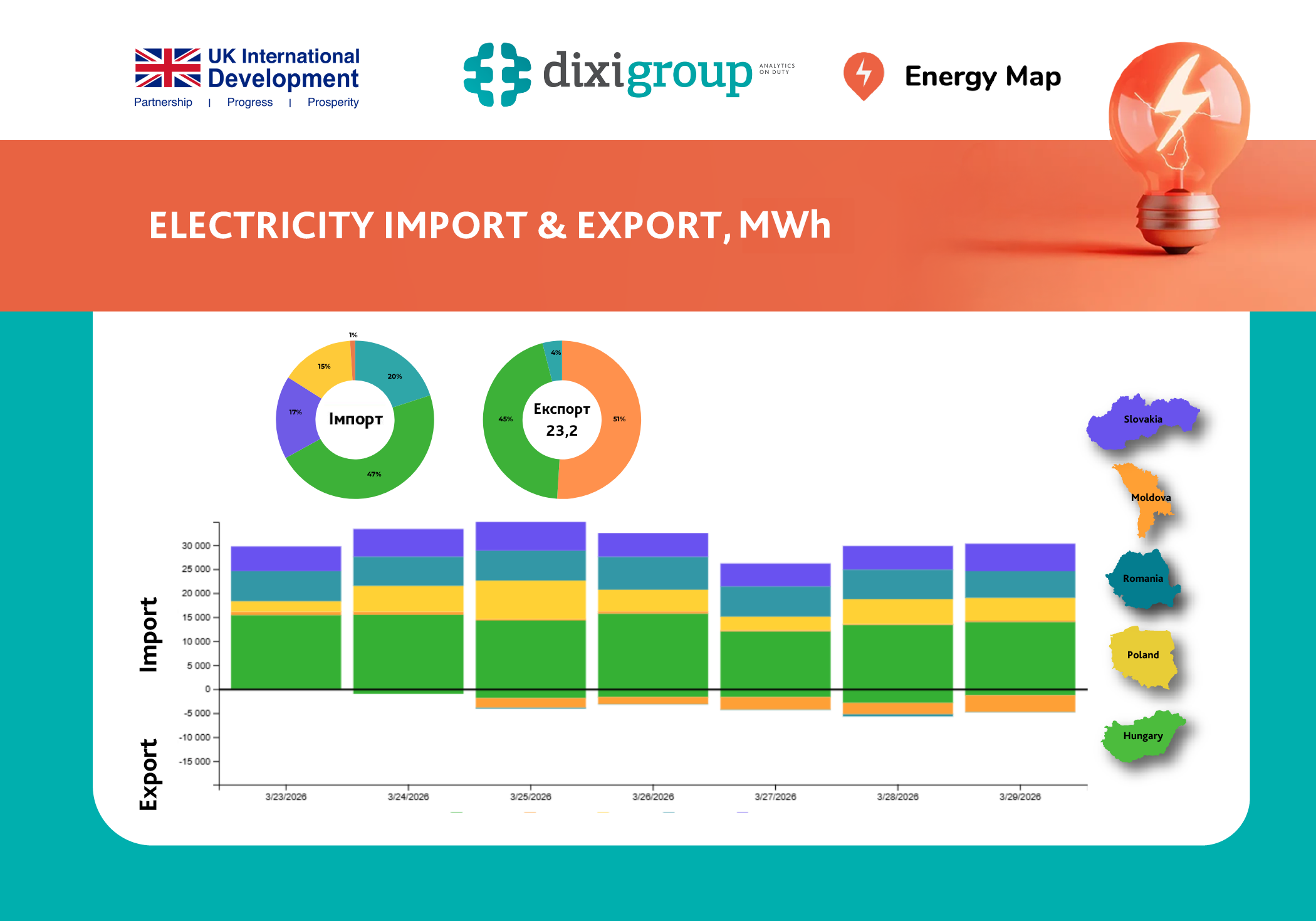

Electricity Import

Imports play a key role in stabilizing the system. In 2024, imports exceeded 4 million MWh, with a peak of 850 thousand MWh in June. In April 2025, imports amounted to 325 thousand MWh. With the approach of the summer season, this volume may increase to 500–800 thousand MWh per month, depending on weather conditions and the risk of new attacks.

“Electricity imports have already become a critical element of energy stability. At the same time, they are an indicator of our integration into the European market, which carries strategic significance,” emphasized Olena Lapenko.

During the presentation, Olena Lapenko outlined three probable scenarios for the summer period:

- The optimistic scenario assumes moderate weather and no large-scale attacks. In this case, peak consumption will not exceed 16 GW, and the available capacity from nuclear, thermal, hydroelectric, and renewable sources will be sufficient to meet demand. The risk of outages will not exceed 5%, provided there are no new damages to generating facilities or the grid.

- The moderate scenario, assuming a hot summer without attacks, anticipates peak load growth to 18–18.5 GW. Even with partial restoration of generation, a deficit of 10–15% may occur. Simultaneously, rising prices on European markets could reduce commercial imports to 1.5 GW, while planned maintenance will lower the availability of domestic capacities.

- The pessimistic scenario accounts for the risk of new attacks on generation. Even with moderate temperatures, the deficit could reach 20% due to significant losses at thermal and hydroelectric power plants—facilities most frequently targeted. The situation is further complicated by limited access to hydro resources and simultaneous maintenance at nuclear and thermal plants.

“The positive scenario appears most likely, but we must be prepared for any developments. Our key priorities are preparing for possible shortages, strengthening infrastructure, and further integrating with the European energy market,” summarized Olena Lapenko.

At the same time, she emphasized that the energy sector’s task is not only to model probable scenarios but to proactively develop effective crisis management solutions. Under martial law, this is not only a matter of efficiency but also national energy security.

Roman Bekuzarov, Deputy Commercial Director at D.TRADING, commented on the functioning of the electricity market during the summer. According to him, the greatest challenge for stable market operation is the significant increase in energy balance profile variability due to growing distributed generation, insufficient export capacity during daytime hours, and limited electricity imports during peak hours caused by price restrictions—price caps. Such imbalance can significantly increase volatility in key market segments such as the Day-Ahead Market (DAM) and Intraday Market (IDM).

“We are already observing how the growth of distributed generation and market restrictions affect stability. During the summer, with increased consumption due to air conditioning and rising base generation from nuclear plants, the situation could become more complicated. The biggest challenge will be balancing the energy system amid daytime surplus and deficits in the mornings and evenings. We are already seeing signs of deficits during these hours on the Day-Ahead Market,” Roman Bekuzarov noted.

Price caps, he said, effectively shift the system balancing responsibility from the market to the operator—NEC Ukrenergo—who is forced to either provide emergency support or impose consumption restrictions. Either full synchronization of price caps with the European market or at least their revision during morning and evening peak hours is needed.

Roman Bekuzarov also noted that the market requires long-term contracts to increase consumption stability and predictability for end-users. This can be achieved through the development of domestic generation as well as through electricity imports. To this end, implementing a mechanism for long-term auctions for access to cross-border interconnections is necessary.

Summer Outlook (Gas): Challenges and Priorities for Summer 2025

In the second part of the event, Olena Lapenko, General Manager for Energy Security and Resilience at DiXi Group, presented a short-term and seasonal adequacy assessment of the gas sector.

According to her, the main task for the summer season is not only to ensure stable gas supply but also to strategically prepare for the upcoming heating season. The key priority is accumulating sufficient volumes of resources as a guarantee of energy security in case of crisis situations.

Gas consumption in 2024 almost matches the 2023 level, especially in the second and third quarters. This indicates a stabilization of demand after a sharp decline in 2022. In 2023, consumption decreased by 2.3% compared to the previous year, partly due to implemented energy efficiency measures. Meanwhile, a slight increase in consumption is expected in the fourth quarter of 2024, caused by increased use of gas for electricity generation amid shortages of other sources.

The situation is complicated by threats to the security of gas infrastructure. In 2023–2024, targeted attacks on extraction and transportation facilities were recorded, limiting storage capabilities. As of mid-May, about 6.14 billion cubic meters of gas have been accumulated in Ukrainian underground gas storage (UGS) facilities. The official target for gas storage accumulation has not been announced, but according to our analytical center’s estimates, it may correspond to at least 14–15 billion cubic meters by November 1, 2025. This exceeds the 13 billion cubic meters accumulated in 2024. These additional volumes are intended to serve as a strategic buffer in case the situation worsens in autumn or winter.

“The dynamics of working gas volumes in Ukraine’s underground storage indicate an unprecedented challenge in 2025. The ‘anti-record’ stock level at the start of the injection season, despite slower withdrawal rates in the 2024/25 season compared to the previous one, requires accelerated resource accumulation considering the risks of infrastructure damage due to military actions. Urgent political decisions are needed regarding funds for gas purchases and establishing new import routes,” emphasized Olena Lapenko.

According to DiXi Group forecasts, gas consumption in 2024 will amount to about 21 billion cubic meters. This volume accounts for decreased demand from households and industry, the impact of hostilities, possible damage to energy infrastructure, as well as increased demand from gas-fired power generation.

Imports remain a critically important source for gas resource accumulation. Since the beginning of 2025, approximately 2 billion cubic meters of gas have been imported. The main supply routes are through Hungary (60% of the total volume), Slovakia (23%), and Poland (17%). Ukraine also has a contract with the Polish company Orlen for the supply of 300 million cubic meters of liquefied gas.

Estimates circulating in the media suggest that total gas imports in 2025 could range from 4 to 8 billion cubic meters. The potential financial burden of procuring this resource is estimated at 2.5–3 billion US dollars. Part of the needs is covered by international partners, including funds from the EBRD and grants from Norway.

Gas Storage Scenarios for Summer–Autumn 2025

As part of its analysis, DiXi Group presented three likely scenarios for gas storage accumulation by the start of the 2025/26 heating season.

- The optimistic scenario foresees accumulating up to 15 billion cubic meters of gas in underground storage by November 1. To achieve this, daily injection rates need to reach about 32 million cubic meters. Imports would amount to up to 5 billion cubic meters. If realized, Ukraine will be well prepared for the winter period even under external challenges.

- The moderate scenario anticipates reaching last year’s level of 13 billion cubic meters. Injection rates would be about 24 million cubic meters per day. Required imports in this case would be around 3.7 billion cubic meters. This scenario covers basic needs but leaves less room for maneuver in case of a crisis.

- The pessimistic scenario predicts accumulating only 11–12 billion cubic meters. Imports would be up to 2 billion cubic meters, with a likely need for additional purchases during winter at higher prices.

“The pessimistic scenario will lead to failing to reach both the target storage level and even the stock level prior to the start of the 2024/25 heating season. This creates a high risk of gas shortages in winter. Key factors include continued intense attacks on infrastructure, difficulties in financing imports, and a significant rise in summer demand due to increased gas-fired generation,” explained Olena Lapenko.

The main risks include declining domestic production, especially in the private sector; insufficient import financing; and weather conditions in October, which may limit injection rates or cause premature demand growth.

Success factors could include concluding long-term contracts ensuring procurement stability; active use of joint purchasing mechanisms to reduce costs; accelerating injection rates starting in June; guaranteed financing through grants, loans, and state guarantees; engaging the private sector by developing exchange trading and a transparent market; as well as modernizing and strengthening infrastructure protection.

According to DiXi Group experts, these measures will help not only to achieve technical targets but also to enhance Ukraine’s overall energy security amid prolonged war conditions.

Artem Petrenko, Executive Director of the Association of Gas Producers of Ukraine, spoke about the state of domestic gas production and consumption in Ukraine, as well as the war’s impact on the industry.

He noted that since the full-scale invasion began, Russia has systematically attacked gas production infrastructure. The sector suffered the greatest losses in February–March 2025, forcing temporary production shutdowns for safety reasons and creating a need for gas imports. Since the beginning of the year, 1.5 billion cubic meters of gas have already been contracted. Additionally, Naftogaz, with government support, has secured €410 million in financing to purchase nearly another 1 billion cubic meters of gas.

“Domestic gas remains the foundation for preparing for the new heating season, so everyone is working at full capacity. Despite challenges and damage, companies are even setting records. For example, Ukrgazvydobuvannya drilled over 107 thousand meters in the first quarter, almost twice as much as in the same period last year,” remarked Artem Petrenko.

At the same time, the market faces challenges. Due to attacks and the imposition of special obligations (PSO) on Ukrnafta, the volume of gas available to the commercial sector has decreased, leading to higher prices for businesses. Petrenko called this market reaction a logical response to shortages. He also highlighted distributed generation, which creates additional gas demand. Some businesses purchase gas at market prices, while others receive it under PSO.

Increasing domestic gas production will remain a priority in the coming years, the association’s head is convinced. Two Production Sharing Agreement (PSA) tenders for the Mezhyhirska and Svichanska blocks have been announced, with tender documentation expected to be published soon. Moreover, Ukrnafta has begun exploratory works at the Oleska block.

“Stable tax policy, clear rules of the game, and predictable resource demand are crucial for further work of producers. These are the main factors for the industry’s development and production growth,” concluded Artem Petrenko.

The material was prepared by DiXi Group with the support of the International Renaissance Foundation as part of the project “Improving the Energy Security of Tomorrow.” The content reflects the authors’ views and does not necessarily represent the position of the International Renaissance Foundation.