The summer season of 2026 is a key stage in Ukraine’s preparations for the 2026/2027 heating season. Unlike the previous season, Ukraine has entered the injection period with a better starting position in terms of gas volumes in UGS facilities; however, this advantage does not eliminate the need for significant additional storage. The government’s baseline target calls for accumulating 14.6 billion cubic meters of gas in UGS facilities by the start of the heating season, while 13.2 billion cubic meters is defined as the minimum required level.

Three components of the gas balance remain critical for meeting demand: domestic production, imports, and stock changes in storage. The key difference in 2026 is that the gas balance is shaped not only by market factors but also by the constant pressure of military risks. This primarily concerns attacks on gas production, transportation, and other related infrastructure. For example, gas production in 2025 fell to 16.97 billion cubic meters, which is more than 10% less than in 2024, although the actual result turned out to be better than expectations following massive attacks on gas production facilities.

Forecast Results

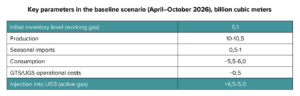

BASE SCENARIO: NO NEW CRITICAL ATTACKS, STABLE IMPORTS

The baseline scenario assumes that during the summer of 2026, there will be no new critical attacks on gas production infrastructure–that is, attacks comparable in impact to the strike of October 3, 2025, after which, according to media estimates, approximately 60% of Ukraine’s gas production was temporarily shut down. Accordingly, this scenario does not anticipate a large-scale, simultaneous loss of production, a significant restriction on UGS operations, or a disruption of key import routes, and Ukraine will be able to maintain access to its main import routes through Poland, Slovakia, Romania, Moldova, and, subject to commercial availability, Hungary.

Key assumptions:

■ no new large-scale attacks on gas production infrastructure and UGS facilities during the summer season;

■ domestic production remains at around 45–50 million cubic meters per day;

■ stable operation of import routes following the technical and commercial reallocation of volumes among different directions;

■ import financing secured through domestic funds, loans, and grants from international partners;

■ the absence of extreme temperature anomalies during the summer and the maintenance of seasonally low consumption levels.

Under the baseline scenario, Ukraine could reach the target level of 14.6 billion cubic meters of gas in UGS facilities by the start of the 2026/2027 heating season. Implementation of this scenario requires a rapid recovery following attacks (mitigating the impact on production figures), minimal imports, and moderate injection rates during the summer season. The average daily increase in reserves should be approximately 35–40 million cubic meters per day, and in certain periods–higher, provided there are sufficient imports and cross-border capacity is available. Achieving these figures will depend on a combination of three factors: stable domestic production, the availability of import routes, and timely financing of gas purchases.

The financial requirements of the baseline scenario will primarily be determined by the cost of imported gas. Assuming an average gas price of 46–48 EUR/MWh, imports of 6.5–7.5 billion cubic meters could require approximately 3.2–3.8 billion EUR just to pay for the gas itself. This estimate is based on a provisional conversion of 1 billion cubic meters of natural gas to approximately 10.55 TWh and does not account for transportation costs, capacity booking, injection, storage, and balancing. A separate component of the financial burden will be the costs of restoring damaged gas infrastructure, which are not included in the cost of imported resources but will affect the sector’s overall financing needs.

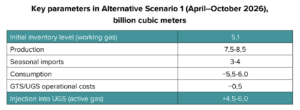

ALTERNATIVE SCENARIO 1: ESCALATING MILITARY RISKS

The first alternative scenario considers a situation in which Russian attacks on gas infrastructure not only continue but also escalate to the level of massive strikes, similar to or more intense than the attack on October 3, 2025. Such a scenario is realistic given the systematic nature of previous strikes on gas production and transmission infrastructure and facilities related to gas storage.

Key assumptions:

■ one or more massive attacks on gas production infrastructure during the summer season, resulting in a prolonged loss of 30–40% of capacity;

■ possible strikes on UGS ground infrastructure, temporarily limiting injection capacity;

■ attacks on GTSOU compressor stations and cross-border interconnection infrastructure, temporarily reducing the throughput capacity of certain routes;

■ maintenance of current import rates with potential expansion through the mobilization of additional financial resources.

In this scenario, Ukraine could technically reach the minimum required level of UGS storage, but the baseline target of 14.6 billion cubic meters depends on timely increases in imports and the availability of external financing for an additional 2–3 billion cubic meters compared to the baseline scenario. Total import demand could rise to 4 billion cubic meters or more, but not all of this volume will necessarily translate into inventory growth: part of the supply may offset domestic demand due to losses in domestic production, increased consumption, technical constraints, or temporary infrastructure disruptions.

If additional funding is not secured in time, Ukraine risks accumulating only 13.2–13.8 billion cubic meters of gas, i.e., at the level of the minimum required reserve or with a slight surplus. This creates a systemic risk, as experience from previous heating seasons shows that initial reserves without a sufficient operational buffer can quickly deplete in the event of cold weather, high consumption, or new attacks on infrastructure.

Precautionary measures for this scenario should include: accelerating gas injection in May–June 2026; expanding credit lines and grant opportunities for Naftogaz to purchase imported gas; more active use of aggregated procurement mechanisms and long-term contracts; building up strategic reserves of equipment for compressor stations and other gas field systems; strengthening the engineering and technical protection of gas infrastructure facilities.

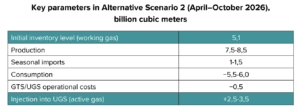

ALTERNATIVE SCENARIO 2: LIMITED IMPORTS AND PRICE SHOCK

The second alternative scenario considers a situation in which an additional constraint for getting through the summer season is not only a physical loss of production but also a deterioration in import conditions. This scenario could materialize if several factors converge: a sharp rise in prices on the European gas market, reduced availability of LNG (due, among other things, to increased competition from Asian buyers), as well as the emergence of additional regulatory, political, or commercial restrictions on certain supply routes.

Key assumptions:

■ all constraints of Alternative Scenario 1;

■ further reduction in global LNG availability or rising prices on the European gas market due to geopolitical escalation, supply disruptions, or increased competition for the resource;

■ as a result, a price shock: the average TTF price during the active injection period rises to 55–65 EUR/MWh;

■ imports lose some of their commercial appeal and occur in limited volumes.

Under this scenario, the expected level of gas reserves as of November 1, 2026, could be 12.3–13.3 billion cubic meters. At the same time, the potential risk lies not in formally failing to reach the minimum stock level, but in reduced operational flexibility compared to the baseline scenario, increased import costs, and vulnerability to additional shocks – such as cold weather, new attacks, or delays in gas supply.

Additional precautionary measures for this scenario should include: active use of transportation schemes with discounts or deferred payment, in particular “short-haul + customs warehouse”; coordination with the EU and other partners regarding Ukraine’s access to LNG supplies in the event of a shortage.

This material was prepared by the NGO “DIXI GROUP” with the support of the International Renaissance Foundation within the framework of the project “Strengthening Ukraine’s Resilience in Energy”. This material reflects the authors’ views and does not necessarily reflect the views of the International Renaissance Foundation.