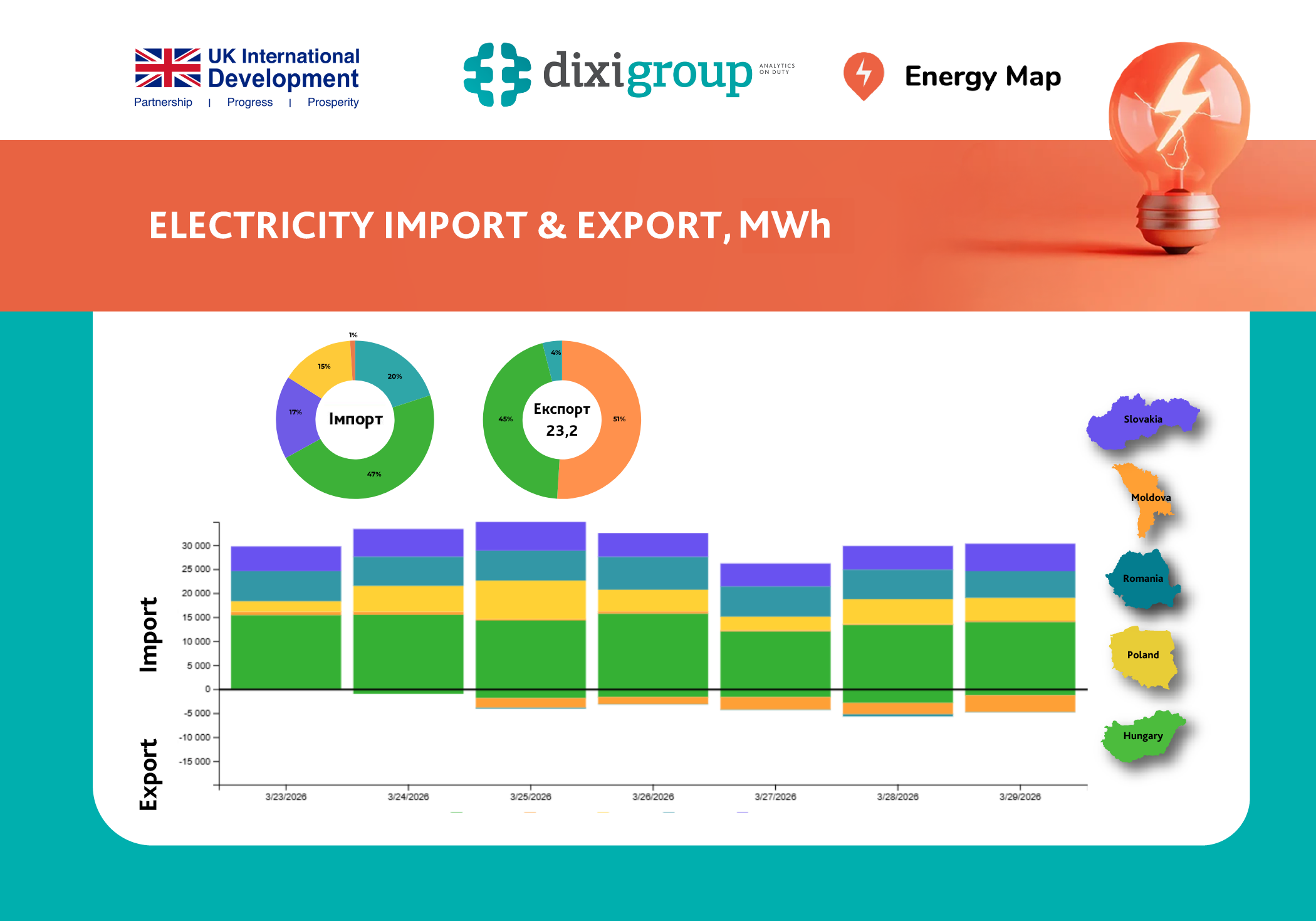

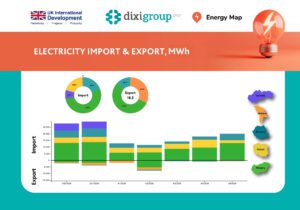

According to Energy Map, between March 30 and April 5, Ukraine reduced electricity imports by 38%, to 133.5 GWh, and exports by 20%, to 18.5 GWh.

One of the reasons for the decline in electricity imports was the change in price caps in the short-term market segments. Starting from April 1, the NEURC reinstated the previous differentiated price caps: in the day-ahead market (DAM) and intraday market (IDM), prices now range from 5 600 to 15 000 UAH per MWh depending on the hour, while in the balancing market they range from 6 600 to 16 000 UAH per MWh. Previously, from January 18 to March 31, the upper limits were uniform: 15 000 UAH per MWh for DAM and IDM, and 16 000 UAH per MWh for the balancing market.

Following the revision of price caps, import volumes decreased to 12.8 GWh on April 1 (-56.3% compared to March 31) and 11.5 GWh on April 2 (-60.5% compared to March 31).

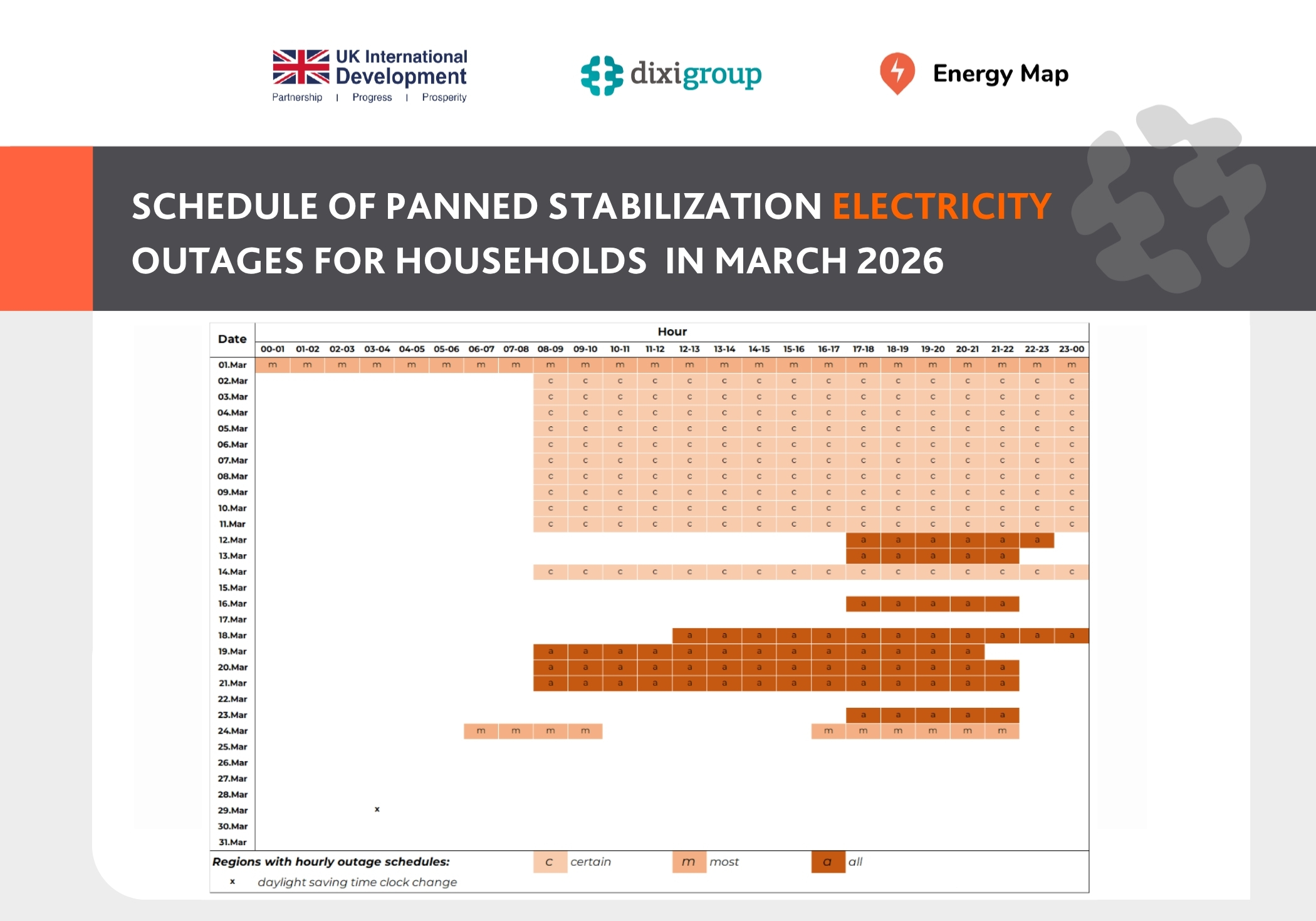

The security situation remains difficult. During the week, russia carried out two massive attacks on the power system, as well as daily localized strikes in frontline and border areas, causing periodic capacity shortages. Balancing is ensured through exports during surplus hours, imports, emergency assistance, as well as consumption restrictions and outages during deficit periods.

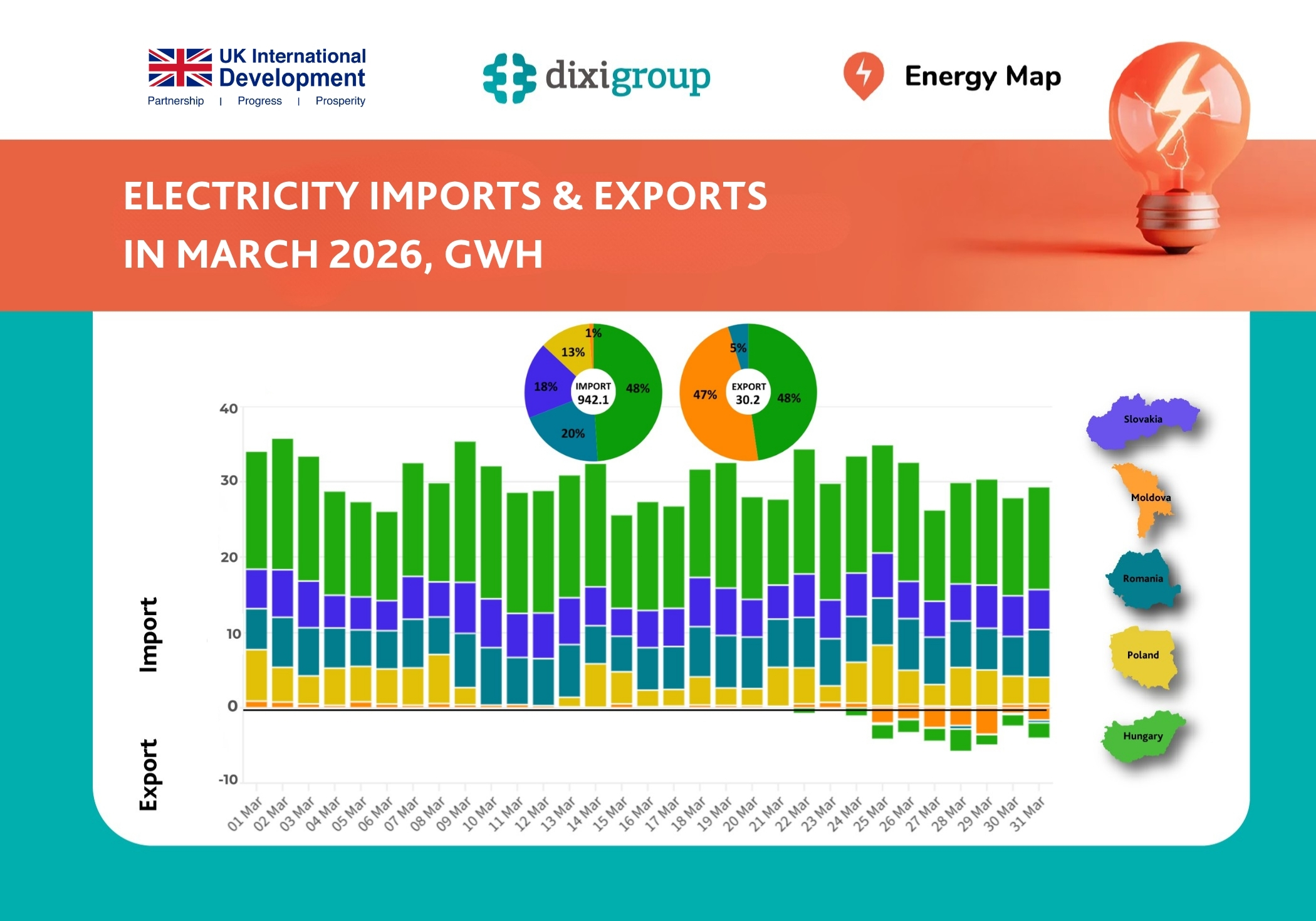

Import structure by country:

- Hungary – 69.2 GWh (51.9%);

- Poland – 26.1 GWh (19.5%);

- Romania – 26.1 GWh (19.5%);

- Slovakia – 10.8 GWh (8.1%);

- Moldova – 1.3 GWh (1.0%).

Electricity imports decreased by 20-71% from all directions.

Export structure by country:

- Hungary – 10.2 GWh (55.3%);

- Moldova – 6.0 GWh (32.3%);

- Romania – 2.3 GWh (12.4%).

There were no deliveries to Slovakia and Poland. Electricity exports to Hungary and Moldova decreased by 1% and 50% respectively, while from Romania they increased by 154%.

The publication was prepared with the financial support of the UK Agency for International Development under the project “Mainstreaming National Energy and Climate Plan for Ukraine’s Green Recovery and Strengthening the Green Transition Office” implemented by DIXI GROUP NGO. The contents of the publication are the sole responsibility of DIXI GROUP NGO and under no circumstances can be considered to reflect the position of the UK Agency for International Development.